Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud. This report includes regional details for Alberta.

Bottom line

Today’s Labour Force Survey data continues to point to a robust labour market in Canada with another strong gains in employment. The slight rise in the unemployment rate to 5.4% resulted from workers returning to the labour market in search of work, suggesting strong confidence in the labour market. Despite the higher unemployment rate, the labour market remains tight, something the Bank of Canada is closely monitoring.

However, the report also shows that wage growth dropped below 4%, with average wages increasing by 3.9% y-o-y, its lowest since early 2022. Moreover, we estimate that the 3-month annualized change of the seasonally-adjusted series, at 1.8%, suggests further deceleration in wage growth.

A robust labour market remains a challenge for the Bank of Canada. While the BoC will welcome the higher unemployment rate, it remains historically low and will need to rise further to create some slack in the labour market. Moreover, wage growth remains disconnected from weak labour productivity.

The continued resilience of the labour market, the strength in the economy, the general lack of slack in the economy and sticky inflation are the main reason supporting another rate hike. On the other hand, there are tentative signs that inflationary pressure could be easing: lower wage growth and inflation excluding mortgage interest payments in line with the BoCès inflation target.

However, the BoC made it clear that it will choose inflation in the tug-of-war between fighting inflation and avoiding a recession. As a result, we believe the BoC will hike its policy rate by 25bp at next week’s meeting, bringing it to 5.00%, and then pause for the rest of the year.

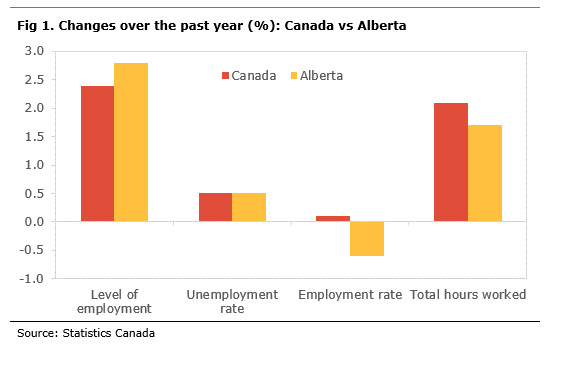

Alberta saw an increase in employment in June, but the unemployment rate remained at 5.7%. Over the past twelve months, the Alberta labour market has outperformed the rest of the country in terms of job gains. However, the unemployment rate in Alberta remains higher than the national measure. As a result, we observe some continued underperformance in wage growth in Alberta at 3.0% y-o-y, compared to 3.9% y-o-y in the rest of Canada.

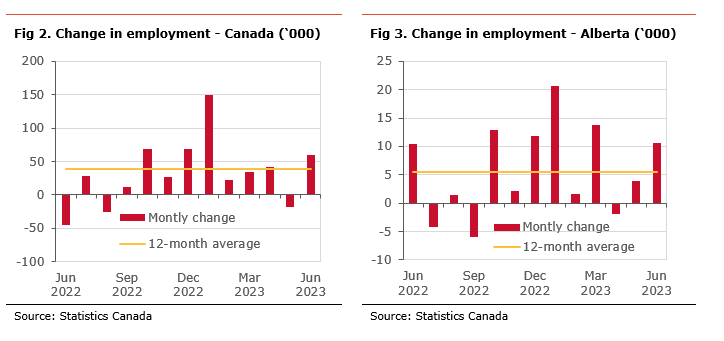

Employment rose by 60.0k in June, after a small decline in May. The details show that part of the strength was from a solid gain in youth employment, partly correcting the decline seen in May.

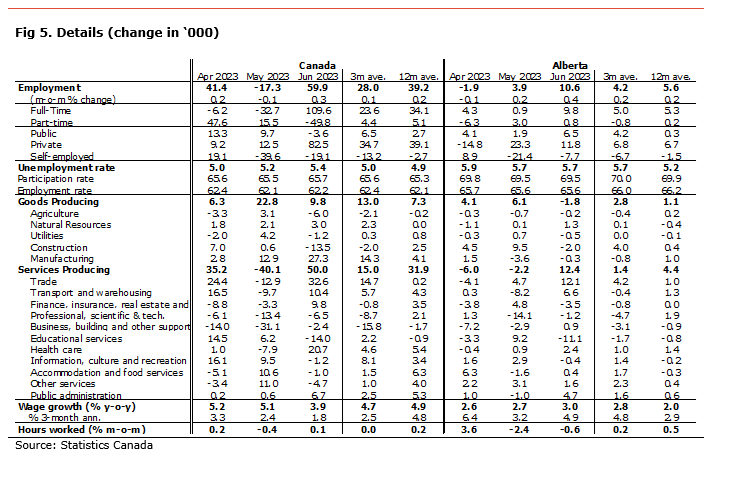

Despite the increase in employment, the unemployment rate rose to 5.4%, its highest level since February 2022 but still historically low. The higher unemployment rate was due to more workers coming into the labour force with the participation rate inching higher to 65.7% from 65.5%. The participation rate is only 0.2 percentage points (pp) lower than before the pandemic, as workers left the labour force. If the participation was the same as before the pandemic, the unemployment rate would be 5.7%. The employment rate, the share of the population holding a job, increased to 62.2%, on par with its pre-COVID level. Wage growth decelerated to 3.9% y-o-y, the lowest since April 2022. The 3-month annualized change in wages almost moderated sharply to 1.8%, suggesting that wage growth is decelerating rapidly.

The details show that the job gains in June were all full-time (+109.6k), while there were losses in part-time (-49.8k). In addition, the increase in employment was mostly in the private sector (+82.5k), while there were losses in self-employed (-19.1k) and the public sector (-3.6k).

On an industrial level, the rise in employment was in bothe the service sector (+50.0k) and the goods-producing sector (+9.8k).

The details in the good-producing sector show that the job gains were mainly in manufacturing (+27.3k). This was partly offset by losses in construction (-13.5k) and agriculture (-6.0k).

The gains in the service industry came mainly from wholesale and retail trade (+32.6k), health care (20.7k), and transport and warehousing (+10.4k), while there were losses in education (-14.0k), professional, technical and scientific (-6.5k), and other services (-4.7k).

Despite continuous gains in employment and the overall level of employment being above its pre-COVID level by 5.1 percentage points, only 12 out of 16 industries have a level of employment above its pre-pandemic level. The lagging sectors are: agriculture, business, building and other support services, accommodation and food services, and other services. Employment in the accommodation and food services is still about 4% below its pre-COVID-19 level, but continues to improve rapidly.

In Alberta, employment increased slightly by 10.6k in May. The participation rate remained unchanged at 69.5% and the unemployment rate edged lower to 5.7%. The participation rate in the province is still 1.6 percentage points (pp) below its pre-pandemic level suggesting many workers are remaining on the sidelines. If the participation rate was at the same level as before the pandemic, the unemployment rate in the province would be 7.8%. The employment rate, the share of the population holding a job, was also unchanged at 65.6%, slightly below its pre-pandemic level.

The job gains in Alberta were mainly in the service sector (+12.4k), while there were modest losses in the goods-producing sector (-1.8k). The decline in the goods-producing industry

was concentrated in construction (-2.0k) and utilities (-0.5k), while there was a small gain in natural resources (+1.3k).

The higher employment in the service sector was mainly in wholesale and retail trade (+12.1k), transport and warehousing (+6.6k), and public administration (+4.7k). These gains were partly offset by losses in education (+11.1k) and finance, insurance and real estate (-3.5k).

Despite the overall employment being above its pre-COVID level by 6.7pp, only 9 out of 16 industries have a level of employment above their pre-pandemic levels. The lagging industries are: agriculture, natural resources, utilities, manufacturing, information, culture and recreation, accommodation and food services, and other services. Employment in the accommodation and food services sector, the worst-hit industry, remains more than 10% below its pre-COVID-19 level, underperforming the rest of the country.

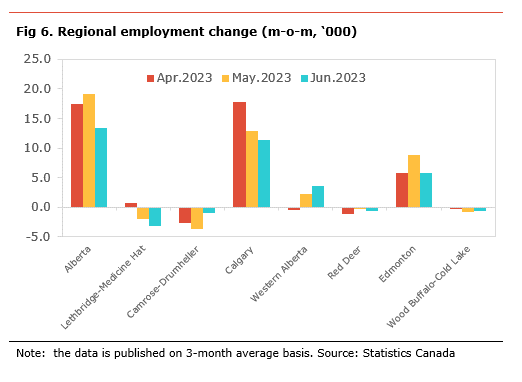

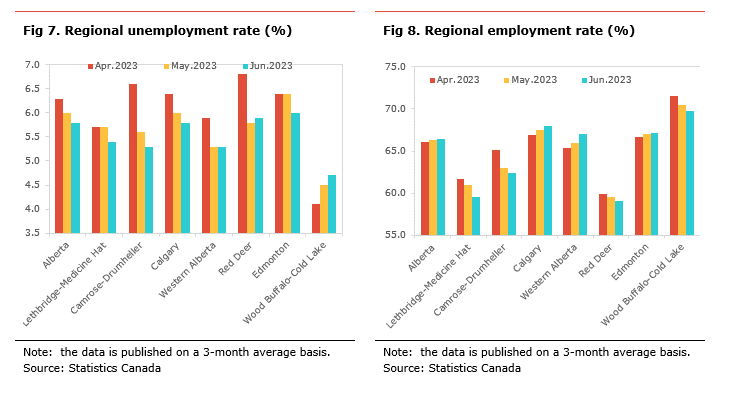

On a regional basis[1], the data is published on a three-month average basis (see table below). Over the past three months, the province gained 13.3k jobs each month on average. Most of the gains were in Calgary (+11.4k) and Edmonton (+5.8k). Conversely, there were declines in Lethbridge-Medicine Hat (-3.2k). With a marginal decrease in May, we note that Red Deer has seen a sixth consecutive decline in employment.

The unemployment rate for the province declined to 5.8% from 6.0%. Most regions saw either unchanged or lower unemployment rates, except for Wood Buffalo-Cold Lake (+0.2pp) and Red Deer (+0.1pp). The biggest declines in the unemployment rate were in Edmonton (-0.4pp), Lethbridge-Medicine Hat (-0.3pp), and Camrose-Drumheller (-0.3pp).

The unemployment rate is the highest in Edmonton (6.0%), Red Deer (+5.9%), Calgary (5.8%), and Red Deer (5.8%). It is the lowest in Wood Buffalo-Cold Lake (4.7%), Western Alberta (5.3%), Camrose-Drumheller (5.3%) and Lethbridge-Medicine Hat (5.4%).

The employment rate for Alberta rose to 66.4% from 66.3%. The employment rate increased the most in Western Alberta (+1.1pp), Calgary (+0.5pp), and Edmonton (+0.1pp). It decreased in Lethbridge-Medicine Hat (-1.4pp), Wood Buffalo-Cold Lake (-0.8pp), Camrose-Drumheller (-0.7pp), and Red Deer (-0.5pp)

[1] All the numbers are expressed as three-month average of the non-seasonally adjusted number.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.