Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

Today’s release of the monthly GDP suggests that the Canadian economy remains robust, after a strong start to 2023. As such, while economic activity was unchanged in April, it was negatively affected by the federal workers’ strike. Moreover, the preliminary estimate for May suggests activity increased 0.4% m-o-m.

The details in April show that sectors linked to consumer discretionary spending, namely retail trade, accommodation and food services, arts, entertainment and recreation, in addition to real estate, remained robust despite the loss in purchasing power due to high inflation and rising debt-service cost. Household spending remains surprisingly resilient and will be key to the outlook, likely supported so far by the strong labour market.

The continued resilience of the Canadian economy will remain a concern for the Bank of Canada, as it suggests that excess demand is not resorbing as fast as they hoped. This would support the case for another rate hike to 5.00% at the July meeting.

For Alberta, the details available in the report suggest that economic activity outperformed slightly the rest of the country in April due to strong activity in the oil and gas sector. High energy prices have been a tailwind to the Alberta economy this year, but not as much as in the past (see Where’s the boom? How the impact of oil on Alberta may have permanently weakened).

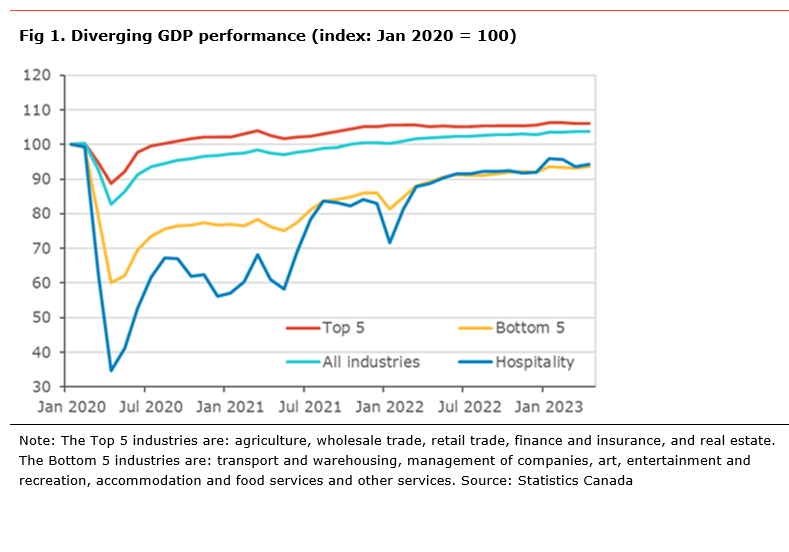

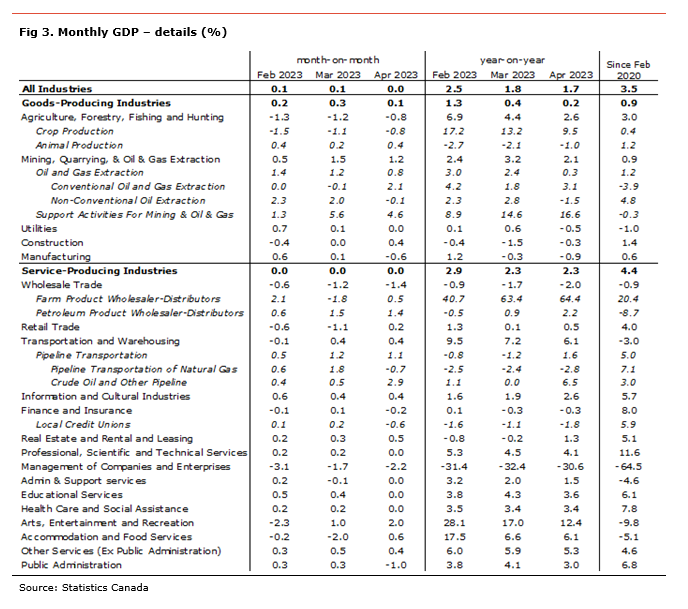

The monthly GDP was unchanged in April (+1.7% y-o-y). The details show that 11 out of 20 industrial sectors posted gains on the month. Despite the overall economy being 3.5 percentage points above its pre-pandemic level, 7 out of 20 industrial sectors still have economic activity below their pre-pandemic levels, namely utilities, wholesale trade, transportation and warehousing, management of companies, administration and support services, arts, entertainment and recreation, and accommodation and food services.

Statistics Canada’s preliminary estimate suggests GDP for May rose by 0.4% m-o-m. This suggests that growth in the second quarter of 2023 could be between 1.5% and 2.0% q-o-q ar.

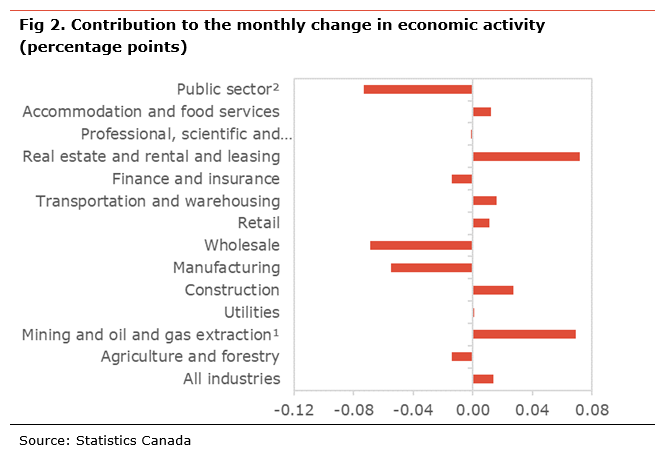

The goods-producing side of the economy increased by 0.1% m-o-m in April. Economic activity was higher in natural resource extractions (+1.2% m-o-m) and construction (+0.4% m-o-m). These increases were partly offset by declines in agriculture (-0.8% m-o-m) and manufacturing (-0.6% m-o-m).

The services-producing side of the economy was flat in April. Activity increased in real estate (+0.5% m-o-m), transportation and warehousing (+0.4% m-o-m), accommodation and food services (+0.6% m-o-m), and retail trade (+0.2% m-o-m). Declines in public administration (-1.0% m-o-m), wholesale trade (-1.4% m-o-m), and finance and insurance (-0.2% m-o-m) were the main drag to growth in the sector. The decline in public administration was the result of the federal public worker strike during the month.

For Alberta, there is no specific data in the report. However, we can make an assessment based on activity in some key industries specific to Alberta. The level of activity in the oil and gas sector rose sharply on the month, especially support activity for mining, oil and gas. A decline in agriculture, the seventh consecutive decline, may also have acted as a drag on growth. An increase in pipeline activity, especially gas pipeline, has provided further support. Overall, this means that the province’s economy likely marginally outperformed the rest of the country in April.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.