Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

Growth in the third quarter came in much stronger than expected, as net exports supported the economic activity due to strong crude oil and agricultural products exports. However, domestic demand contracted for the first time since 2021Q2, showing that the domestic economy is stalling and feeling the impact of the rate hikes and the decline in household purchasing power. As such, residential investment and consumer spending were a significant drag on growth.

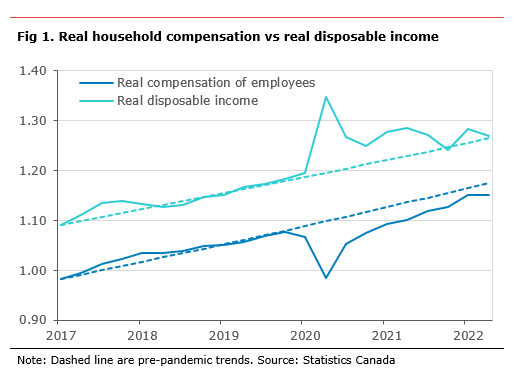

Both employee compensation and disposable income improve in the second quarter. However, once adjusted for inflation, real disposable income was lower, leading to a continued decline in purchasing power. The saving rate surprisingly increased slightly, suggesting that households could be more cautious with their spending than initially thought. With inflation remaining high and interest rates continuing to rise, households face continued pressures on their purchasing power and finances.

We expect economic activity to slow in the last quarter of 2022 as the sharp increases in interest rates continue to take their toll on economic activity, especially residential investment and consumer spending. How strong consumer spending will depend on households’ willingness to spend the money saved during the pandemic, especially as inflation erodes households’ purchasing power and higher interest rates lead to higher debt-service payments.

Today’s GDP number does not change our view that the BoC will hike by 25bp at the December meeting. While growth was more robust than expected, most of the strength comes from likely one-off increases in exports. Moreover, a weakening domestic economy suggests that previous rate hikes are having the intended impact on the economy.

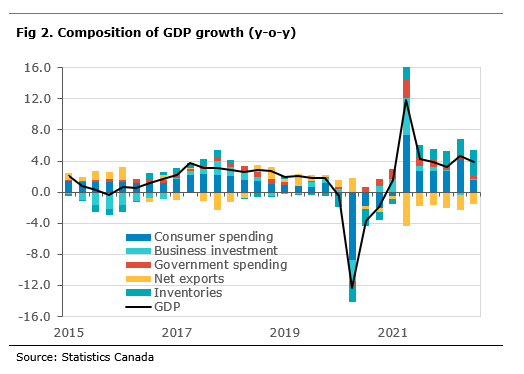

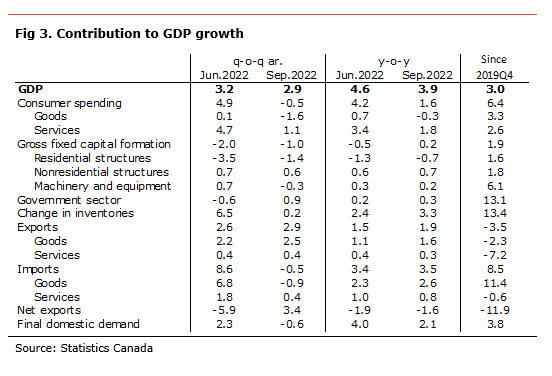

The Canadian economy grew by 2.9% q-o-q annual rate (ar) in the third quarter of 2022 (+3.9% y-o-y), much stronger than expected. This followed an increase of 3.2% q-o-q ar. in the second quarter of 2022. Two years after the start of the pandemic, economic activity stands 3.0% above its pre-pandemic level.

In terms of details, a large proportion of the rise in economic activity can be attributed to a strong increase in net exports (contributing 3.4 percentage points (pp) to growth, while residential investment (subtracting 1.4pp from growth) and consumer spending (subtracting 0.5pp from growth) contracted on the quarter. Final domestic demand contracted for the first time since 2021Q2, when COVID-related restrictions were reintroduced.

Household spending declined by 5.1% q-o-q ar, reducing growth by 1.2pp. This followed a robust 3.2% q-o-q ar. rise in the second quarter of 2022. Spending on services remained robust, rising by 3.8% q-o-q ar., contributing 1.1pp to growth. Spending on goods decreased by 1.6% q-o-q ar., removing 0.3pp to growth. The decline in spending was fairly broad-based affected almost equally durable, semi-durable and non-durable goods.

Business investment contracted by 1.0% q-o-q ar. on the quarter, reducing growth by 1.0pp to growth. The details show a big decline in residential investment, while investment in machinery and equipment and non-residential structures increased.

Residential investment dropped by 15.4% q-o-q ar., subtracting 1.4pp to growth. The reduction in activity in the sector was broad-based with contractions in new construction, renovation activity and ownership transfer costs.

Business investment in non-residential structures increased 11.7% q-o-q ar., contributing 0.6pp to growth, as a result of an increase in engineering structures as spending at the Kitimat LNG project and solar projects in Alberta continued in the third quarter. Investment machinery and equipment edged lower by 4.0% q-o-q ar., removing 0.3pp to growth.

The external sector was the main source of growth, adding 3.4pp to growth. Exports of goods and services increased 8.6% q-o-q ar. in Q3, contributing 2.8pp to growth, led by exports of crude oil and farm products. Imports declined by 1.5% q-o-q ar., contributing 0.5pp to growth.

Canada’s terms-of-trade deteriorated in Q3 (-6.3% q-o-q) mainly as a result of a decline in crude oil prices and other commodities. Nevertheless, the terms-of-trade remains close to record. A continued high level of the terms-of-trade will positively affect Alberta and other oil-producing provinces.

On the income side, household disposable income rose by 0.8% q-o-q. The higher disposable income was due to a 1.2% q-o-q rise in employees’ compensation. However, the compensation of employees has increased at its slowest pace since it declined at the start of the pandemic.

With consumer spending contracting while disposable income continued to increase, the household saving rate increased to 5.7% from 5.1%, still well above its pre-pandemic level.

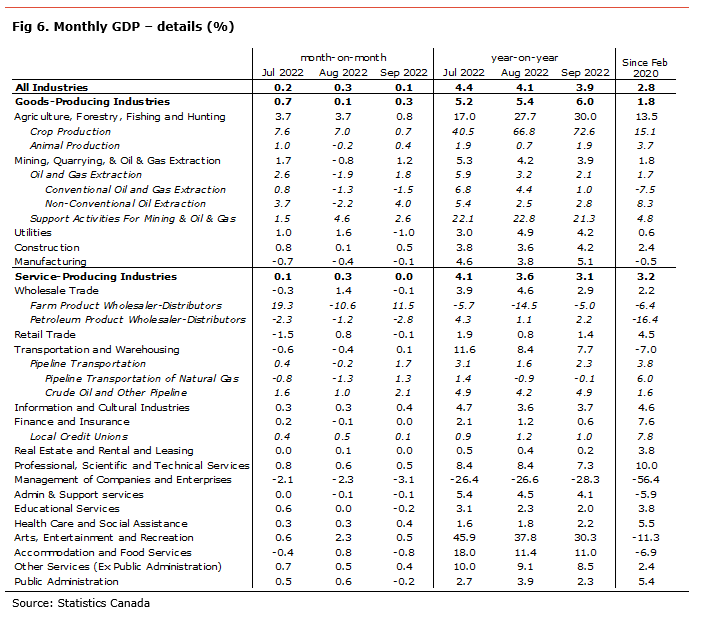

The monthly GDP for September rose by 0.1% m-o-m (+4.7% y-o-y). The preliminary estimate for October suggests that activity was likely unchanged m-o-m.

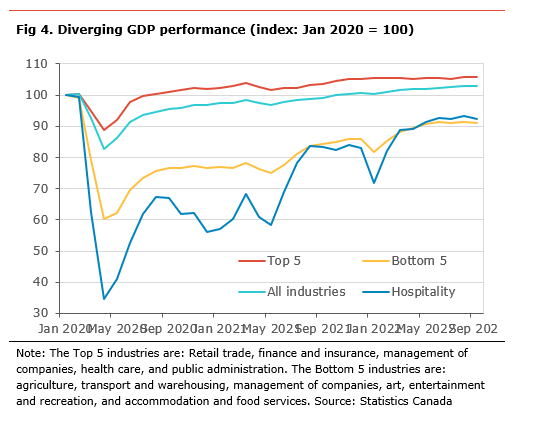

The level of economic activity is 2.8% above its pre-pandemic level. Only 14 out of 20 industrial sectors have economic activity above pre-pandemic levels, with manufacturing, transportation and warehousing, management of companies, administration and support, arts, entertainment and recreation, and accommodation and food services are still below their pre-pandemic level.

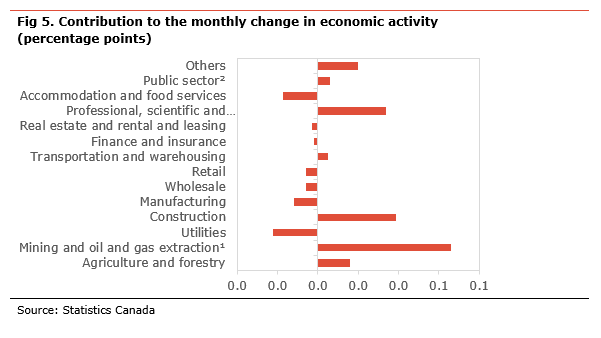

The goods-producing sector rose 0.3% m-o-m (+6.0% y-o-y), mainly due to the mining, oil and gas sector, agriculture and construction. A decline in manufacturing and utilities partly offset those increases. The service sector was flat on the month (+3.1% y-o-y). The performance of the sector was mixed. Increases in professional, scientific and technical services, arts, entertainment and recreation, and health care were offset by declines in accommodation and food services, retail trade and public administration.

For Alberta, there is no specific data in the report. However, we can make an assessment based on activity in some key industries specific to Alberta. The activity level increased on the month in oil and gas extraction, agriculture, and pipeline transportation. This suggests that the level of economic activity in the province was likely stronger than in the rest of the country in September.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.