Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

Inflation accelerated to 4.0% in August, more than expected. The higher inflation rate is largely the result of higher gasoline prices and shelter costs, especially mortgage interest payments, rent and electricity costs. More importantly, all measures of underlying inflationary pressures accelerated in August, suggesting increased stickiness in inflation.

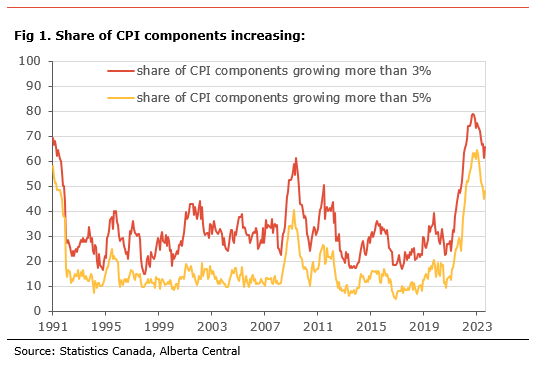

Inflationary pressures also broadened, with 48% of the components of CPI rising at more than 5%, compared to 45% in July. Similarly, the share of components increasing by more than 3% increased to 66% (see Fig 1.). The reversal of previous progress in the reduction in the percentage of components rising by more than 3% and 5% will be a disappointment for the Bank of Canada and suggests a widening of the distribution of y-o-y increases.

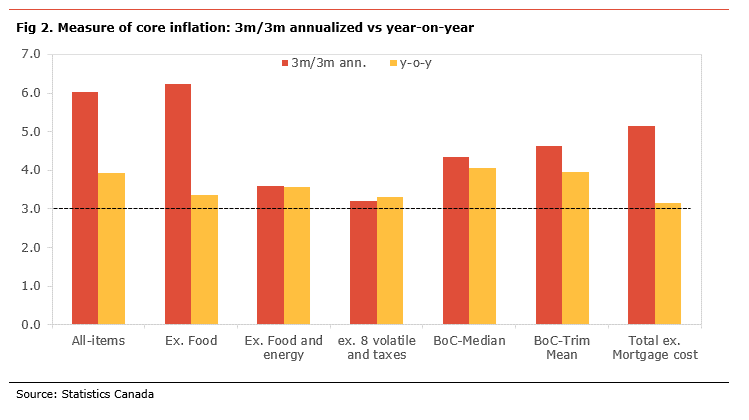

The recent trend in CPI’s monthly changes suggests that the momentum in inflationary pressures rose in August. As such, we can observe that many of the 3-month annualized changes in some key CPI components (shelter and transportation) are higher than the year-on-year changes, suggesting further acceleration in those components. (see Fig. 2). The 3-month annualized changes in headline CPI is now at 6.0%, its highest since August 2022. Similarly, the same measure for the BoC’s core measures increased 4.5% on average, its highest since July 2022, suggesting continued strong price pressures. CPI excluding food and energy is at 3.6%, also above the BoC’s target range, while it is 3.2% for the BoC’s old measure of core (CPI ex the 8 most volatile components and indirect taxes).

The broad reacceleration in most measures of core inflation will be a worry for the BoC. More particularly, the fact that inflation momentum, as measured by the 3-month annualized changes, in many core measures are at their highest in over a year suggests that inflation could be reaccelerating or proving much sticker at best.

With oil prices and gasoline prices remaining higher than last year, headline inflation is expected to average almost 4% for the rest of the year. The question for the BoC will be what the second-round impact of higher energy prices will be on underlying inflationary pressures, and core inflation is likely to remain stickier than the central bank anticipated.

The increased stickiness in core measures of inflation raises the probability that the BoC may increase its policy rate before the end of the year. The decision continues hinges on whether the domestic economy slows, reducing excess demand, and whether we see some moderation in inflationary pressures. With this in mind, the next CPI release and Labour Force Survey may prove key.

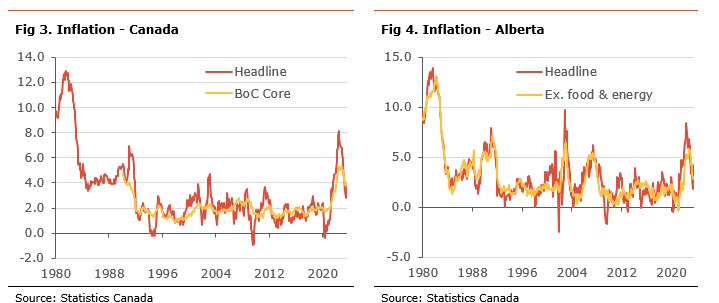

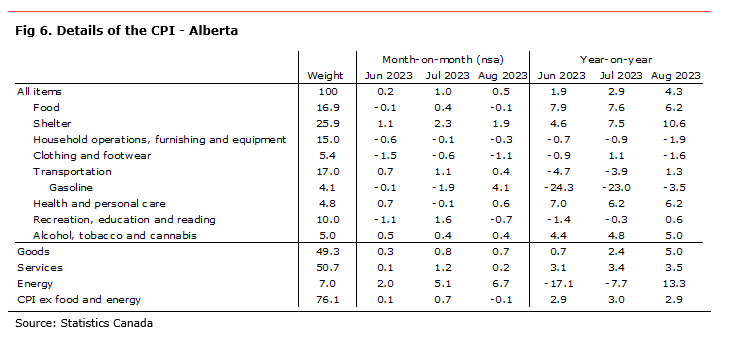

In Alberta, inflation jumped to 4.3%. The sharp rise was mainly due to an acceleration in shelter costs, contributing 2.7pp percentage points to inflation. Food prices decelerated and remained one of the main sources of inflation. Inflation excluding food and energy (a measure of core inflation) inched lower to 2.9% and remained below the national measure.

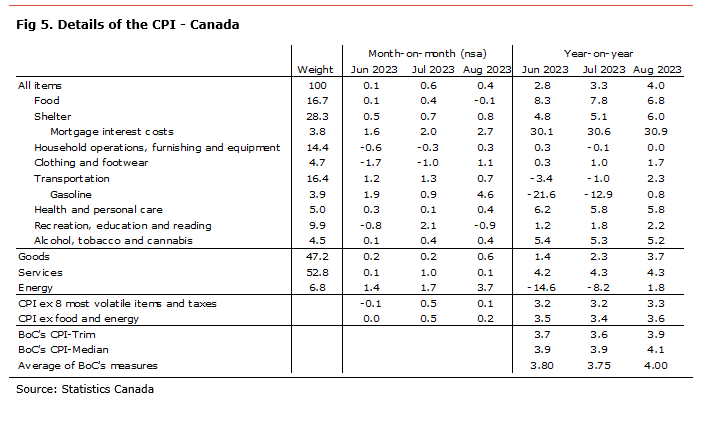

The Consumer Price Index (CPI) increased by 0.4% m-o-m non-seasonally-adjusted in August and the inflation rate accelerated to 4.0%. This was above expectations. Prices rose on the month in six of the eight major CPI components, led by clothing and footwear(+1.1% m-o-m). Shelter costs were up by 0.8%, due to higher mortgage interest rate costs (+2.7% m-o-m) and rents (+0.&% m-o-m). Transportation rose +0.7% m-o-m, due to a 4.6% m-o-m increase in gasoline prices. Food prices eased 0.1% m-o-m in August, while recreation, education and reading declined (-0.9% m-o-m), due to lower travel service costs (-4.1% m-o-m).

Six of the eight major CPI components decelerated in August on a year-on-year basis. Shelter costs accelerated to 6.0% and is the main source of inflation, contributing 1.7 percentage points (pp), with about 1.17pp attributable to higher mortgage interest costs and 0.4pp due to higher rent. A continued rise in electricity cost (+1.5% m-o-m and +12.3% y-o-y) due to higher prices in Alberta was also an important source of pressure on shelter costs.

Food prices remained one of the main sources of inflation, but eased to 6.8% y-o-y, the lowest since February 2022, contributing 1.1pp to inflation. Transportation costs increased 2.3% y-o-y, adding 0.4pp to inflation, with gasoline prices no longer acting as a drag on inflation by rising 0.8% y-o-y.

In August, goods prices inflation accelerated to 3.7% from 2.3%, while services inflation were unchanged at 4.3%. Energy prices rose 1.8% y-o-y compared to the same month last year, the first y-o-y increase since January 2023. Excluding food and energy, prices rose 0.2% on the month and by 3.6% compared to the same month last year. The Bank of Canada’s old measure of core inflation, CPI excluding the 8 most volatile components and indirect taxes, was edged higher to 3.3%.

Looking at the BoC’s core measures of inflation, all indicators accelerated in August. CPI-Trim rose to 3.9% from 3.6% and CPI-Median to 3.9% from 4.1%. As a result, the average of the two measures increased to 4.00% from 3.75%.

In Alberta, inflation jumped to 4.3% in August from 2.9%. The main source of inflation acceleration was transportation costs, which rose 1.3% y-o-y after a decline of 3.9% y-o-y the previous month due to higher gasoline prices. Shelter costs rose 10.6% y-o-y and remain the main source of inflation, contributing 2.7pp to inflation. A continued increase in electricity cost (+11.1% m-o-m and +121.7% y-o-y) remained a significant source of inflation with owned accommodation costs and rent. Food prices decelerated to 6.2% y-o-y and remained an important source of inflation in the province, contributing 1.0pp to inflation.

Goods prices inflation jumped to 5.0% from 2.4%, while services prices rose to 3.5% from 3.4%. Inflation excluding food and energy edged lower to 2.9%, while energy costs rose 13.3% y-o-y.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.