Economic commentary provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

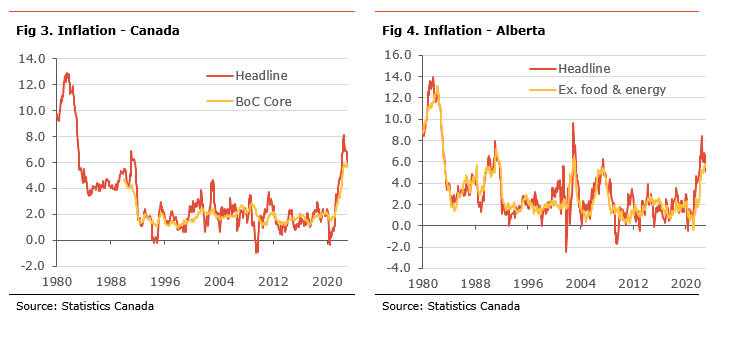

Inflation moderated more than expected in January but remained elevated at 5.9%. Some of the moderation results from a base effect and moderation in mobile phone service costs and slower increase for motor vehicles. There are some signs of modest moderation in underlying inflationary pressures, with most measures of core inflation easing slightly in January yet remaining elevated.

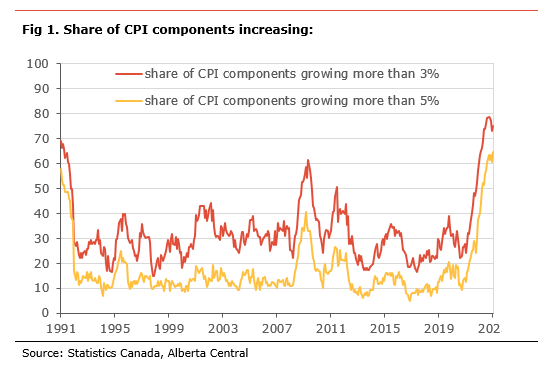

Inflationary pressures remain broad, with 75% of the components of CPI rising at more than 3% y-o-y, and more than 60% at more than 5% y-o-y (see Fig 1). The share of CPI components rising by more than 3% and by more than 5% increased slightly in January. This suggests a slight broadening in inflationary pressures despite the lower level of core inflation. The lack of narrowing in inflationary pressures may catch the attention of the Bank of Canada, as it suggests that the easing in headline and core inflation is, so far, mainly the result of a small subset of items.

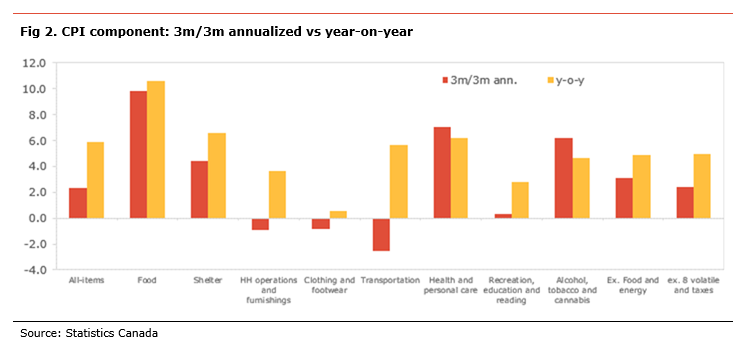

The recent trend in the CPI monthly changes suggests that inflationary pressures are losing some momentum in recent months. The 3-month annualized change in most CPI components decelerated and remains below their year-on-year changes, suggesting that inflation should continue to moderate (see Fig. 2). The 3-month annualized changes in headline CPI is now at 2.4%, within the BoC’s target band, and it is only slightly above 3% for CPI ex. food and energy (3.1%). This suggests that the recent inflation dynamic is broadly consistent with the BoC target

While inflation has peaked and is moderating, it remains well above the BoC’s target of 2%, inflation expectations are elevated, and inflationary pressures remain broad and sticky. Nevertheless, the BoC will welcome an inflation dynamic, as measured by the 3-month annualized changes, that is consistent with inflation converging toward the upper band of its inflation target. In our view, this supports the case for the BoC to continue its conditional commitment to leave its policy rate unchanged.

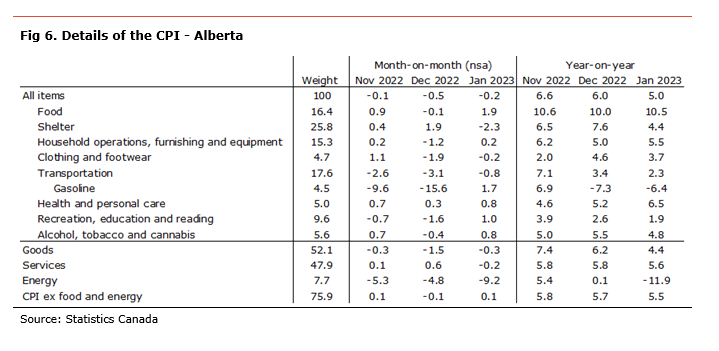

In Alberta, inflation declined to 5.0%. A sharp deceleration in electricity costs and gasoline prices y-o-y, as a result of rebates as part of the Affordability Action Plan, was the main cause of the decline in inflation, while a continued rise in food prices was the main source of inflation. Inflation excluding food and energy (a measure of core inflation) eased to 5.5%. We note that core inflation in Alberta remains above the rest of the country.

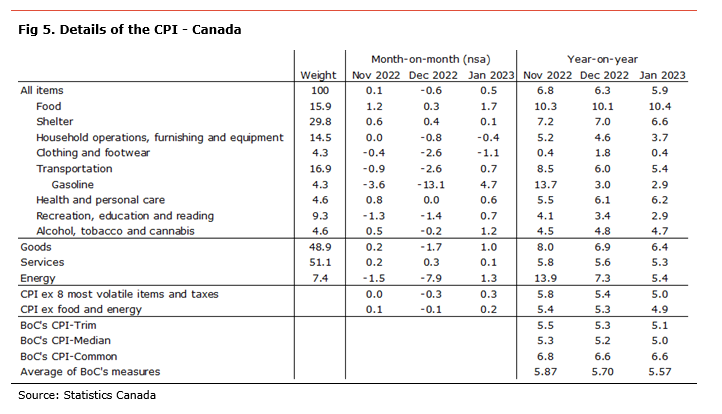

The Consumer Price Index (CPI) increased by 0.5% m-o-m non-seasonally-adjusted in January and the inflation rate moderated to 5.9%, both weaker than expectations. Prices rose on the month in six of the eight major CPI components, led by food prices (+1.7% m-o-m), alcohol, tobacco and cannabis (+1.2% m-o-m), and transportation cost (0.7% m-o-m), due to an increase in gasoline price (+4.7% m-o-m). Prices declined for clothing and footwear (-1.1% m-o-m) and household operations, furnishing and equipment (-0.4% m-o-m). Shelter cost rose a modest 0.1% m-o-m, as a decline in utilities costs (-0.6% m-o-m) offset the rise in mortgage interest costs (+2.6% m-o-m).

Six of the eight major CPI components decelerated in January on a year-on-year basis. Shelter costs decelerated to 6.6% and remain the main source of inflation, contributing 2.0 percentage points (pp), with about 0.6pp attributable to higher mortgage interest costs. Transportation costs decelerated to 5.4% y-o-y, contributing 0.9pp to inflation, with passenger vehicle prices being the source of the slower pace of increase. Household operation costs grew at a slower pace of 3.7% y-o-y, contributing 0.5pp to inflation, as mobile phone services and child care costs declined compared to last year. Food prices accelerated to 10.4% y-o-y, the highest since August 1981, contributing 1.7pp to inflation. Prices at the grocery, especially for meat, continued to be the main source of price pressures.

In December, goods prices inflation decelerated to 6.4% from 6.9% and services inflation moderated to 4.9% from 5.3%. Energy prices decelerated to 5.4% y-o-y from 7.3% y-o-y. Excluding food and energy, prices decreased 0.2% on the month and rose by 4.9% compared to the same month last year, marking a deceleration. The Bank of Canada’s old measure of core inflation, CPI excluding the 8 most volatile components and indirect taxes, was eased to 5.0%.

Looking at the BoC’s core measures of inflation, two out of three indicators decelerated in January. CPI-Median eased to 5.0% from 5.2%, CPI-Trim to 5.1% from 5.3%, while CPI-Common remained unchanged at 6.6%.

In Alberta, inflation moderated to 5.0% in January from 6.0%. Shelter costs were the main source of the decline in inflation and increased 4.4% y-o-y, compared to 7.6% y-o-y in December, contributing 1.1pp to inflation. The sharp deceleration was the result of the rebate on electricity put in place as part of the Affordability Action Plan. Transportation costs also moderated to 2.3% y-o-, contributing 0.4pp to inflation as a result of a decline in gasoline prices compared to last year due to the tax rebate. On the flip side, food prices accelerated to 10.5% y-o-y, the highest since 2001, contributing 1.7pp to inflation. Household operations, furnishing and equipment costs also accelerated to 5.5% y-o-y, contributing 0.8pp to inflation due to a sharp increase in household furnishing and equipment prices.

Goods price inflation decelerated to 4.4% from 6.2%, while services prices eased to 5.6% from 5.8%. Inflation excluding food and energy eased to 5.5%, while energy costs dropped substantially (-11.9% y-o-y) compared to the same month last year, as a result of lower gasoline and electricity prices. This is the first y-o-y decline in energy prices since August 2020.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.