Economic commentary provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

Housing activity declined in September for a third consecutive month, while national house prices fell for the first time since March. The decline in housing activity comes after the Bank of Canada increased its policy rate in June and July. Moreover, some recovery in inventories nationally will provide some needed slack into the housing market and hold back prices.

In Alberta, housing market activity remained very robust by historical standards. However, we note a continued divergence between the metropolitan areas. Prices in Calgary have continued to increase over the past year, and the city remains one of the strongest housing markets in Canada, supported by low inventories and strong population growth. On the flip side, Edmonton, while showing some sign of improvement, continues to underperform as inventories remain higher. Strong migration into Alberta and affordability are major supports for activity and prices compared to elsewhere in the country.

Low interest rates have been one of the main drivers of the housing market in recent years, supporting affordability. The latest rise in interest rates is pushing affordability to be at its lowest in decades in many cities. After a rebound earlier this year, it is clear that the 50bp increase by the Bank of Canada in June and June is cooling the housing demand. The question is whether it will rebound once households adjust to the new reality as they did earlier this year. The continued lack of supply in many regions and increased immigration will likely support house prices and prevent a big correction, with the health of the labour market likely the key to the outlook for the housing market.

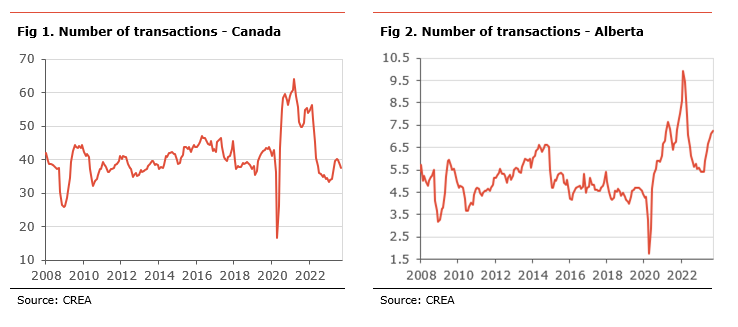

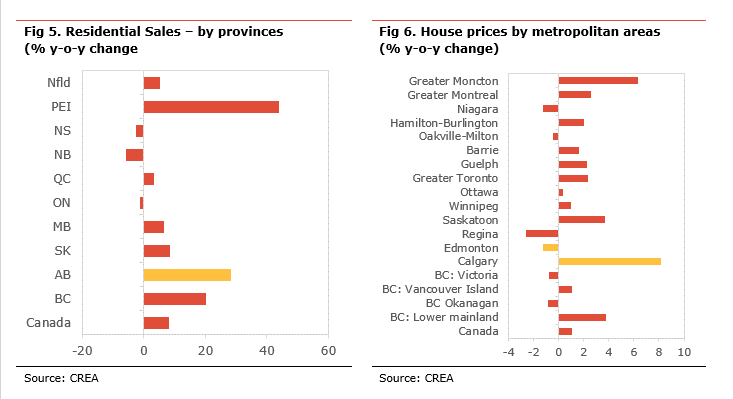

Activity in the Canadian housing market eased by 1.9% m-o-m seasonally-adjusted in September. As a result, the number of transactions, at 37.7k, is 8.1% higher than for the same month last year. In September, activity was lower in almost all provinces, except in PEI (+3.7% m-o-m) and Alberta (+1.9% m-o-m). Activity declined the most in New Brunswick (-11.2% m-o-m), BC (-4.1% m-o-m), Saskatchewan (-4.1% m-o-m), Newfoundland (-3.5% m-o-m), and Ontario (-3.0% m-o-m).

There continue to be some divergences between provincial markets. Compared to the average level of 2019, the number of transactions is well above its pre-pandemic level in Alberta (+63%), Saskatchewan (+39%), and Newfoundland (+39%). On the flip side, activity is well below in Ontario (-27%), Quebec (-17%), Nova Scotia (-16%), and New Brunswick (-7%).

New listings rose 6.3% m-o-m seasonally-adjusted in September, a sixth consecutive month of increase. New listings increased in most provinces, with the biggest gains in Nova Scotia, Ontario, New Brunswick, and BC.

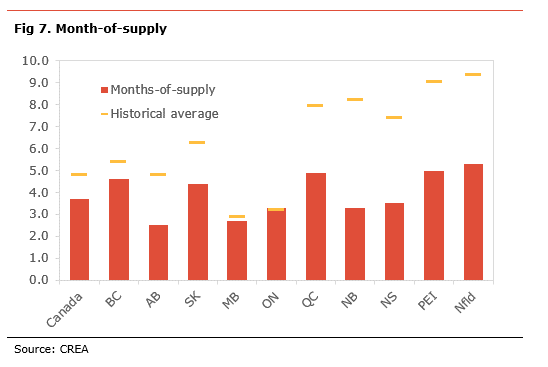

With sales activity being weaker than new listings in most regions, the month-of-supply measure[1] was edged higher to 3.7 nationally, but still slightly lower than at the start of year. Based on this measure, BC, Ontario, New Brunswick and Nova Scotia saw the biggest increase in inventories in September, while it declined in PEI and Newfoundland.

Compared to the highest level of inventory reached during the recent housing market correction, the month-of-supply has decreased the most in PEI (2.2 months), Newfoundland (2.2 months), Saskatchewan (1.7 months), and Alberta (-1.4 months).

With a month-of-supply at 2.5, Alberta’s housing market is at its tightest since 2007, if we exclude the pandemic.

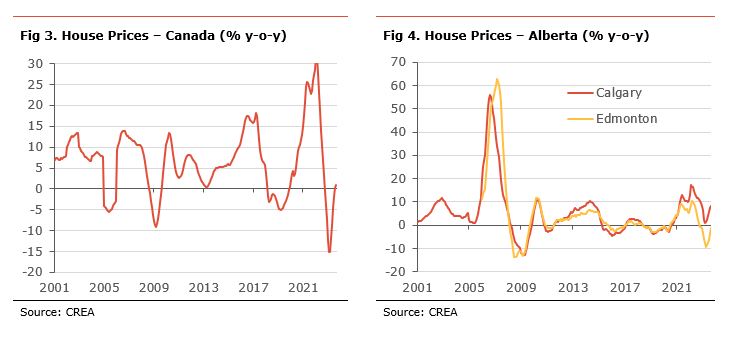

With reduced sales and higher inventories, the MLS House Price Index eased by 0.3% m-o-m, the first decline in price since March 2023. Compared to last year, house prices nationally have increased by 1.8% y-o-y.

The biggest monthly price decreases were in Oakville-Milton (-3.9% m-o-m), Okanagan (-3.1% m-o-m), Greater Toronto (-0.8% m-o-m), Regina (-0.6% m-o-m), and Hamilton-Burlington (-0.5% m-o-m). Prices increased the most in Saskatoon (+1.5% m-o-m), Vancouver Island (+1.2% m-o-m), Calgary (+1.0% m-o-m), and Edmonton (+1.0% m-o-m).

On a y-o-y basis, most regions have seen higher prices, with the most significant increases in Calgary (+8.2% y-o-y), Moncton (+6.3% y-o-y), BC Lower Mainland (+3.8% y-o-y), and Saskatoon (+3.7% y-o-y). Prices declined compared to last year in Regina (-2.6% y-o-y), Edmonton (-1.2% y-o-y), Niagara (-1.2% y-o-y), and Okanagan (-0.9% y-o-y).

Compared to their recent peaks, prices have declined by 9.9% nationally. However, prices are still almost 40% higher than they were in January 2020 on the eve of the pandemic. Compared to their recent peak, prices dropped the most in Oakville-Milton (-16%), Hamilton-Burlington (-16%), Niagara (-15%), Barrie (-14%), Guelph (-14%), Toronto (-10%), Okanagan (-8%), and Ottawa (-8%).

Prices have corrected the least in Montreal (-2.6%), and Winnipeg (-4.3%). Prices have not declined in Calgary, Saskatoon and Moncton.

In Alberta, benchmark prices rose 1.0% m-o-m and are up 8.2% y-o-y in Calgary and by 1.0% m-o-m and -1.2 % y-o-y in Edmonton. There continues to be a divergence between the performance in Edmonton and Calgary, likely resulting from continued higher inventories in Edmonton. However, the gap between both cities is narrowing.

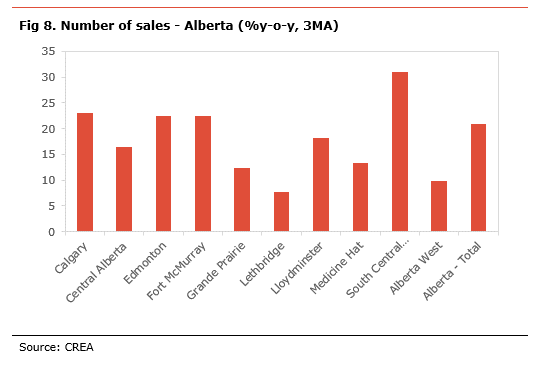

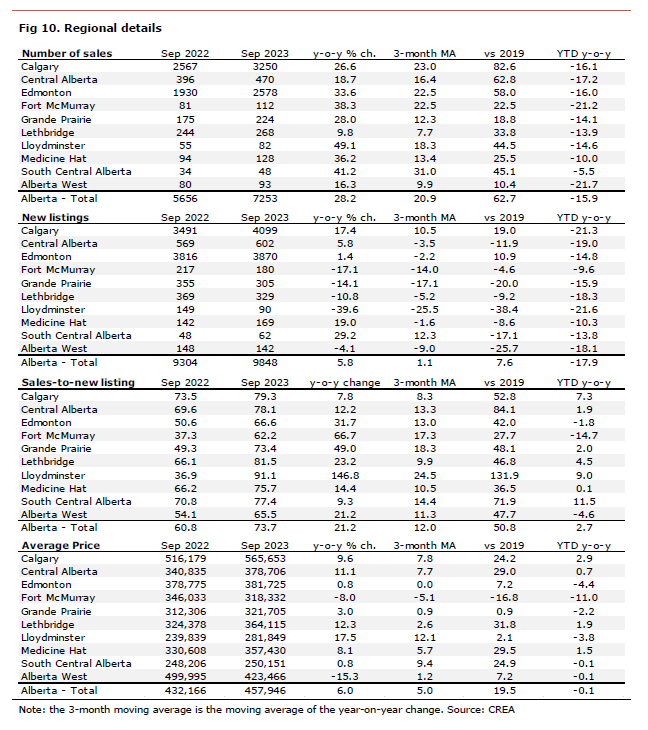

In Alberta, the housing market remains robust, with transactions still well above their pre-pandemic level. The number of transactions has increased in all regions compared to last year’s same month. (see table below for details). Compared to the average level of transactions in 2019, activity in the province increased by 63%, led by Calgary (+83%), Central Alberta (+63%), Edmonton (58%), South Central Alberta (+45%), Lloydminster (+45%), and Lethbridge (+34%).

New listings increased in September and compared to the same month last year at the provincial level. However, there were some important declines in inventories in Grande Prairie (-23% y-o-y), South Central Alberta (-22% y-o-y), and Lloydminster (-20% y-o-y). Compared to the average level of new listings in 2019, new supply in the province increased by 76% and was lower in most regions except in Calgary and Edmonton. New listings declined the most compared to 2019 in Lloydminster (-38%), Alberta West (-26%), Grande Prairie (-20%), and South Central Alberta (-17%).

With sales stronger than new listings in recent months, many regions have seen a tightening of their housing markets. The primary seller’s markets are South Central Alberta, Calgary, Lethbridge, Central Alberta, and Medicine Hat. The main buyer’s markets are Fort McMurray, Edmonton, Alberta West, and Lloydminster.

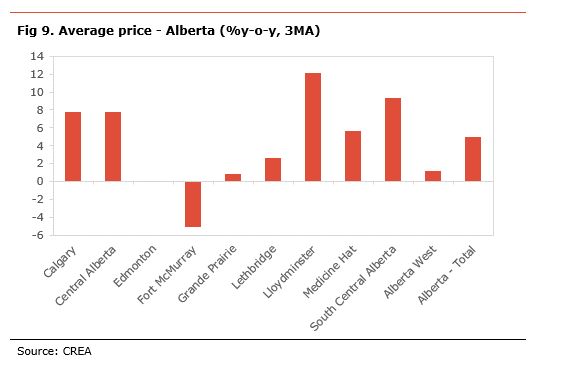

Average house prices increased by 4.3% on a 3-month moving average of the year-on-year in the province. Prices increased the most in Alberta West (+7.6%), Calgary (+6.9%), South Central Alberta (+6.5%), and Central Alberta (+5.4%). However, prices declined over the same period in Fort McMurray (-8.21%), Grande Prairie (-1.9%), and Edmonton (-1.1%).

[1] The month of supply measures how many months is would take at current sales volume and without an increase in listings to bring inventories to 0.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.