Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

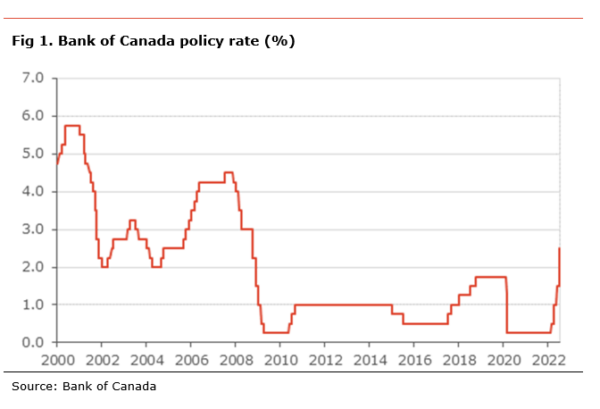

The Bank of Canada increased its policy rate by 100bp to 2.50%, more than expected and its highest level since October 2008. This is the biggest increase at a monetary policy meeting since August 1998 during the Asian Financial crisis. The central bank also announced that it will continue quantitative tightening (QT).

The key message in today’s decision is that the central bank is fully committed to controlling inflation. The decision to front-load the increase in policy rate is an effort to nip in the bud any upside pressure on inflation expectations and prevent the high inflation rate from becoming entrenched. It also suggests that when deciding between bringing down inflation or avoiding a recession, the BoC will prioritize inflation. This means that the BoC will likely remain unphazed by the current pullback in the housing market unless it threatens financial stability.

Overall, today’s decision shows the BoC will remain aggressive to lower inflation and prevent a de-anchoring of inflation expectations. We believe that this means another 50bp hike at the September meetings and likely 50bp at the October meeting, ending the year at 3.5%. Of course, some of those increases could be front-loaded depending on incoming inflation numbers. QT will also play a role and could substitute for some of the rate increases that could be required later this year or next.

It is important to stress that the BoC has little control over global inflationary pressures coming from higher commodity prices or global supply chain disruptions. As such, increasing interest rates will not lower food or gasoline prices or make the computer chip shortage disappear. The only way for the BoC to lower inflation is by slowing the domestic economy, creating excess capacity and reducing domestic inflationary pressures. This is a balancing act that will lead to a period of economic underperformance, notably in the labour market and consumer spending. Whether it will be a soft-landing or a recession remains to be determined.

The BoC increased its policy rate by 100bp to 2.50%, more than expected. It also announced it would continue its policy of quantitative tightening, in line with our expectations. The statement makes it clear that the central bank decided to front-load interest rate increases In addition, it is clear that further rate hikes should be expected, saying “with the economy clearly in excess demand, inflation high and broadening, and more businesses and consumers expecting high inflation to persist for longer, (…), the Governing Council continues to judge that interest rates will need to rise further.” The communiqué also warns that the central bank stands ready to act more aggressively if needed to return inflation back to the 2% target.

The BoC view inflation as remaining around 8% for the next few months. While the BoC continues to view that “global factors such as the war in Ukraine and ongoing supply disruptions have been the biggest drivers”, it is clear that the central bank is becoming increasingly concerned by the broadening of domestic inflation given the rise in core inflation and “more than half of the components that make up the CPI are now rising by more than 5%.” The BoC also notes that inflation expectations are rising, leading to inflation becoming entrenched.

The BoC views that further excess demand has built up in the Canadian economy, fueling domestic inflation. The central bank notes that “labour markets are tight with a record low unemployment rate, widespread labour shortages, and increasing wage pressures” and that “with strong demand, businesses are passing on higher input and labour costs by raising prices”. The central bank also notes that a sharp slowdown in the housing market comes after unsustainable strength in the post-pandemic area.

The Boc downgraded its outlook for the Canadian economy in its Monetary Policy Report significantly. As such, its latest forecast shows the economy growing more modestly, with growth expected at 3.5% in 2022, 1.8% in 2023, and 2.4% in 2024. This compares to expectations of 4.2%, 3.2% and 2.2%, respectively, in the April MPR. Despite weaker growth, inflation is expected to by higher than previously thought at 7.2% in 2022, 4.6% in 2023 and 2.3 in 2024, compared to 5.3%, 2.8% and 2.1%, respectively.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.

Alberta Central member credit unions can download a copy of this report in the Members Area here.