Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud.

Bottom line

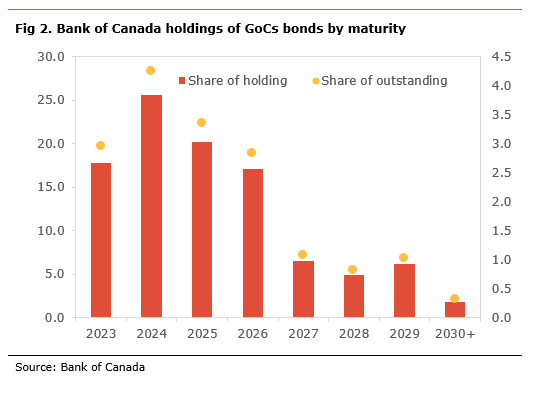

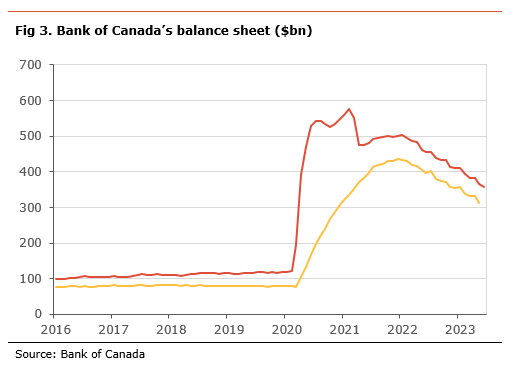

The Bank of Canada hiked its policy rate to 5.00% and will also continue quantitative tightening (QT). This was in line with our expectations.

The key message in today’s decision is that the BoC is concerned by the persistence of both excess demand in the economy, with continued strong domestic demand and a tight labour market despite the significant monetary tightening since early 2022. As a result, core inflation is proving more persistent than the BoC had expected, supporting the BoC’s decision to tighten monetary policy further.

We also believe that concerns regarding its reputation may also be playing a role in tilting the balance toward further hikes. The BoC has been under intense scrutiny and criticism for having left interest rates too low for too long during the recovery from the pandemic and being partly responsible for the current high inflation. By acting aggressively, the Bank is likely trying to restore its credibility as an inflation fighter and influence inflation expectations. As a result, the BoC likely prefers to do too much, rather than not enough.

While the Boc does not provide any forward guidance on whether further rate hikes could be necessary, suggesting that the BoC will be data-dependant. Nevertheless, it is clear that if there were a tug-of-war between economic activity and fighting inflation, the BoC would choose the fight against inflation. With this in mind, while we believe that the BoC is likely on the sideline for the rest of the year, further rate increases this year cannot be ruled out. They would depend on the evolution of inflationary pressures and whether excess demand remains persistent.

The BoC hikes its policy rate by 0.25bp to 5.00%, as expected. It also continued its quantitative tightening policy. In its statement, the BoC says that more persistent excess demand and elevated core inflation justified the need for another increase in the policy rate. The central bank did not provide any guidance as to whether it believes further hikes will be needed. However, the Bank mentions that it will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target”. The BoC also makes it clear that it “remains resolute in its commitment to restoring price stability for Canadians”, suggesting that it stands ready to act decisively if inflationary pressures do not ease and remain stubbornly sticky.

The BoC sees global inflation easing, mainly due to lower energy prices and slower gain in goods prices, while robust demand and tight labour markets are leading to more persistent services inflation. The Bank notes that growth in the US has been stronger than expected, thanks to the resilience of consumer and business spending, while the Chinese economy is softening, and the growth in the Euro Area is effectively stalled. Overall, global growth was revised higher for both 2023 and 2024, at 2.8% and 2.4%, respectively, and to grow by 2.7% in 2025.

The Canadian economy has been stronger than expected, with more momentum in demand, especially consumer spending. The BoC “expects consumer spending to slow in response to the cumulative increase in interest rates”, but recent indicators suggest excess demand will be more persistent than expected. The BoC notes that the labour market remains tight and wage growth remains elevated. The central bank also notes that strong population growth is feeding both the demand and supply side of the economy. The BoC revised higher its growth forecast for 2023 to 1.8% from 1.4%, but lowered it for 2024 and 2025 to 1.2% and 2.4%, respectively. The Bank now expects excess demand to resorb itself in early 2024.

The BoC is concerned that. While inflation has moderated thanks to lower energy prices, momentum in core inflation remains elevated.. The Bank notes that “with three-month rates of core inflation running around 3½-4% since last September, underlying price pressures appear to be more persistent than anticipated.” The BoC now expects inflation “to hover around 3% for the next year before gradually declining to 2% in the middle of 2025. This is a slower return to target than was forecast in the January and April projections.”

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.