Economic insight provided by Alberta Central Chief Economist Charles St-Arnaud. This report includes regional details for Alberta.

Bottom line: Today’s Labour Force Survey data suggest the labour market in Canada remains strong, despite the weakness observed over the summer months. The low unemployment rate continues to signal that the labour market remains very tight, which the Bank of Canada is closely monitoring. Moreover, the report also shows that wage growth continues to accelerate, with average wages increasing by 5.6% y-o-y.

The resilience in the labour market supports the Bank of Canada’s view that further rate increases will be needed to control inflation. As we have explained on numerous occasions, the Bank of Canada needs to slow growth and create some excess capacity in the economy to fight inflation. This will likely lead to a rise in the unemployment rate and to job losses. With that in mind, a weakening of the labour market would be a welcomed outcome for the BoC.

The outlook for the policy rate remains dependent on incoming inflation numbers and we continue to believe that the BoC will hike its policy rate by 25bp in December. However, the strength and the continued tight labour market increase the risk that the BoC could raise rates by 50bp instead if inflation remains strong.

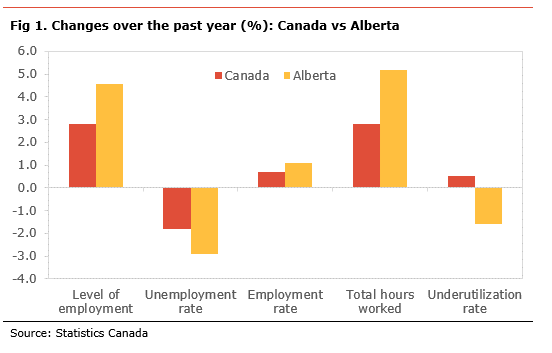

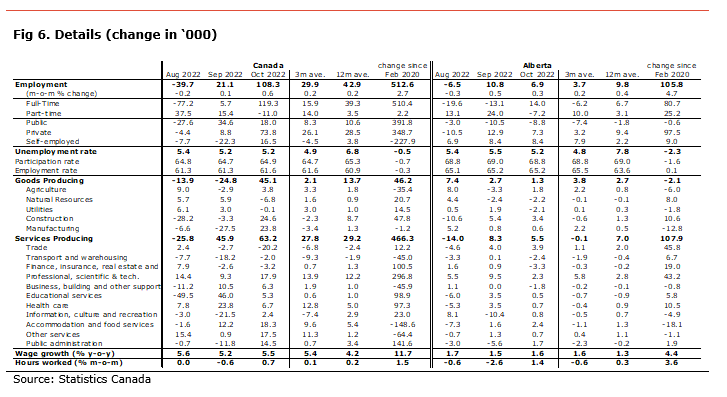

Alberta saw a smaller increase in employment in October than in the rest of the country. However, the unemployment rate eased to 5.2%, as some workers opted to leave the labour market. Over the past year, Alberta’s labour market has outperformed the rest of the country. However, it is important to note that the low unemployment rate is partly the result of workers having left the labour market, as shown by the participation rate remaining below its pre-pandemic level. As such, if the participation rate was the same as before the pandemic, the unemployment rate in the province would be much higher at 7.2%.

Employment rose by 108.3k in October, well above expectations, and reversing the job losses seen over the summer months. Despite the surge in employment, the unemployment rate remained unchanged at 5.2% as a result fo an increase in the participation rate to 64.9% from 64.7%. The participation is 0.7 percentage points (pp) lower than before the pandemic, as workers left the labour force. If the participation was the same as before the pandemic, the unemployment rate would be 5.7%. The employment rate, the share of the population holding a job, rose to 61.6% from 61.3%, still slightly below its pre-COVID level.

The details show that the job gains in October were mostly full-time (+119.3k), while there was a small loss in part-time jobs (-11.0k). In addition, the rise in employment was mainly in the private sector (+74k) and public sector jobs (+18k) and self-employed (+16.5k).

On an industrial level, the increase in employment was in both the service sector (+63k) and in the goods-producing sector (+45k).

The details in the good-producing sector show that most of the job gains were in manufacturing (+28k) and construction (+25k). There were also some small declines in natural resources (-7k).

The gain in the service industry was mainly in accommodation and food (+18k), professional, scientific and technical services (+18k), other services (+17.5k) and public administration (+14.5k). These gains were partly offset by losses in trade (-20k), finance, insurance and real estate (-3k) and transport and warehousing (-2k). Over the past 12 months, employment in the professional, scientific and technical services has increased by almost 300k, representing almost 60% of the job gains over the period.

Despite the overall level of employment being above its pre-COVID level, only 10 out of 16 industries have a level of employment above its pre-pandemic level. The lagging sectors are: agriculture, manufacturing, transport and warehousing, business, building and other support services, accommodation and food services, and other services. Employment in the accommodation and food services is still more than 10% below its pre-COVID-19 level.

In Alberta, employment increased by 6.9k in October. Despite the most gain in employment, the unemployment rate eased to 5.2% from 5.5%. This is the result of a decrease in the participation rate to 68.8% from 69.0%. The participation rate in the province is still 1.6d percentage points (pp) below its pre-pandemic level suggesting many workers are remaining on the sidelines. If the participation rate was at the same level as before the pandemic, the unemployment rate in the province would be 7.2%. The employment rate, the share of the population holding a job, was unchanged at 65.2, on par with its pre-pandemic level.

The job gains in Alberta were in both the goods-producing sector (+1.3k) and the service sector (+5.5k). The gains in the goods-producing industry were in construction (+3k) and agriculture (+2k). These gains were partly offset by declines in natural resources (-2k) and utilities (-2k).

The job performance in the service sector was mixed. There were gains in trade (+4k), accommodation and food services (+2k), professional, scientific and technical services (+2k), and public administration (+2k). These increases were partly offset by losses in finance, insurance and real estate (-3k) and transport and warehousing (-2k).

Despite overall employment being above its pre-COVID level, only 9 out of 16 industries have a level of employment above its pre-pandemic level. The lagging industries are: agriculture, utilities, manufacturing, business, building and other support services, information, culture and recreation, accommodation and food services, and other services. Employment in the accommodation and food services sector, the worst-hit industry, remains almost 20% below its pre-COVID-19 level. Employment in the manufacturing sector is more than 10% below its pre-covid level, significantly underperforming the rest of the country.

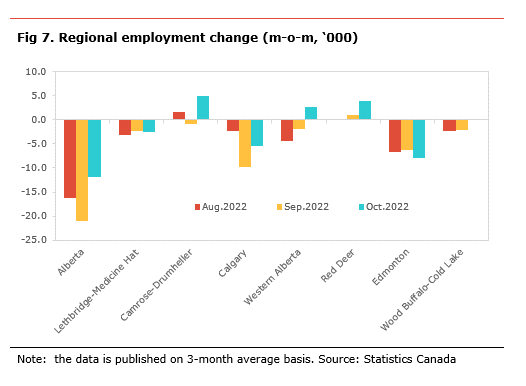

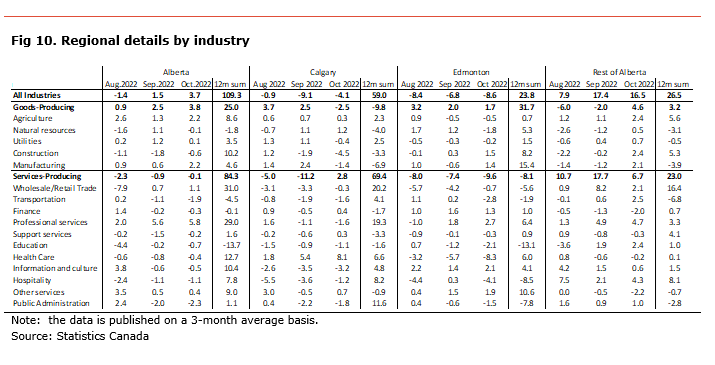

On a regional basis[1], the data is published on a three-month average basis (see table below). Over the past three months, the province lost 11.9k jobs, with employment declining in Edmonton (-8.0k), Calgary (-5.4k), and Lethbridge-Medicine Hat (-2.6k). There were gains in Camrose-Drumheller (+5.0k), Red Deer (+4.0k) and Western Alberta (+2.8k).

Compared to the pre-pandemic levels, Calgary (+9.0%), Edmonton (+4.7%) and Red Deer (+1.6%) are the only regions where employment is higher. In comparison, employment in Wood Buffalo-Cold Lake (-5.3%) and Lethbridge-Medicine Hat (-4.8%) are still well below their pre-covid level.

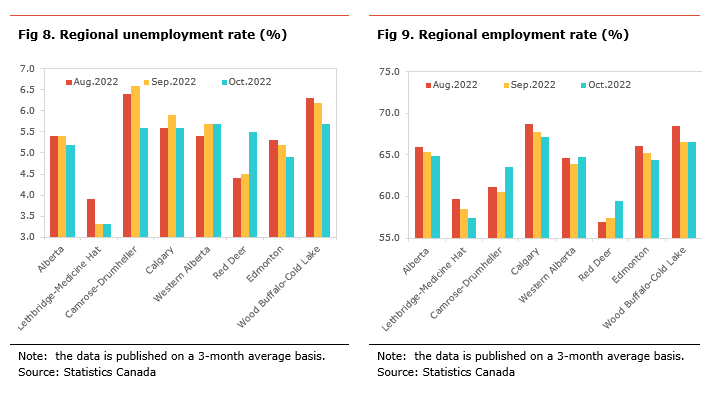

The unemployment rate for the province inched lower to 5.2%, but the regional performance was mixed. The unemployment rate declined in Camrose-Drumheller (-1.0pp), Wood Buffalo-Cold Lake (-0.5pp), Edmonton (-0.3pp) and Calgary (-0.3pp), while it increased in Red Deer (+1.0pp).

The unemployment rate is the highest in Wood Buffalo-Cold Lake (5.7%), Western Alberta (+5.7%), Camrose-Drumheller (+5.6%), and Calgary (+5.6%). It is the lowest in Lethbridge-Medicine Hat (3.3%), Edmonton (4.9%), and Red Deer (5.4%).

The employment rate for Alberta declined to 64.9% from 65.4%. The employment rate decreased the most in Lethbridge-Medicine Hat (-1.1pp), Edmonton (-0.8pp), and Calgary (-0.5pp). It increased in Camrose-Drumheller (+3.0pp), Red Deer (+2.0pp), and Western Alberta (+0.9pp).

[1] All the numbers are expressed as three-month average of the non-seasonally adjusted number.

Independent Opinion

The views and opinions expressed in this publication are solely and independently those of the author and do not necessarily reflect the views and opinions of any organization or person in any way affiliated with the author including, without limitation, any current or past employers of the author. While reasonable effort was taken to ensure the information and analysis in this publication is accurate, it has been prepared solely for general informational purposes. There are no warranties or representations being provided with respect to the accuracy and completeness of the content in this publication. Nothing in this publication should be construed as providing professional advice on the matters discussed. The author does not assume any liability arising from any form of reliance on this publication.